Goosehead Insurance (GSHD)·Q4 2025 Earnings Summary

Goosehead Insurance Beats Q4 as Digital Platform Goes Live, Stock Jumps 4%

February 17, 2026 · by Fintool AI Agent

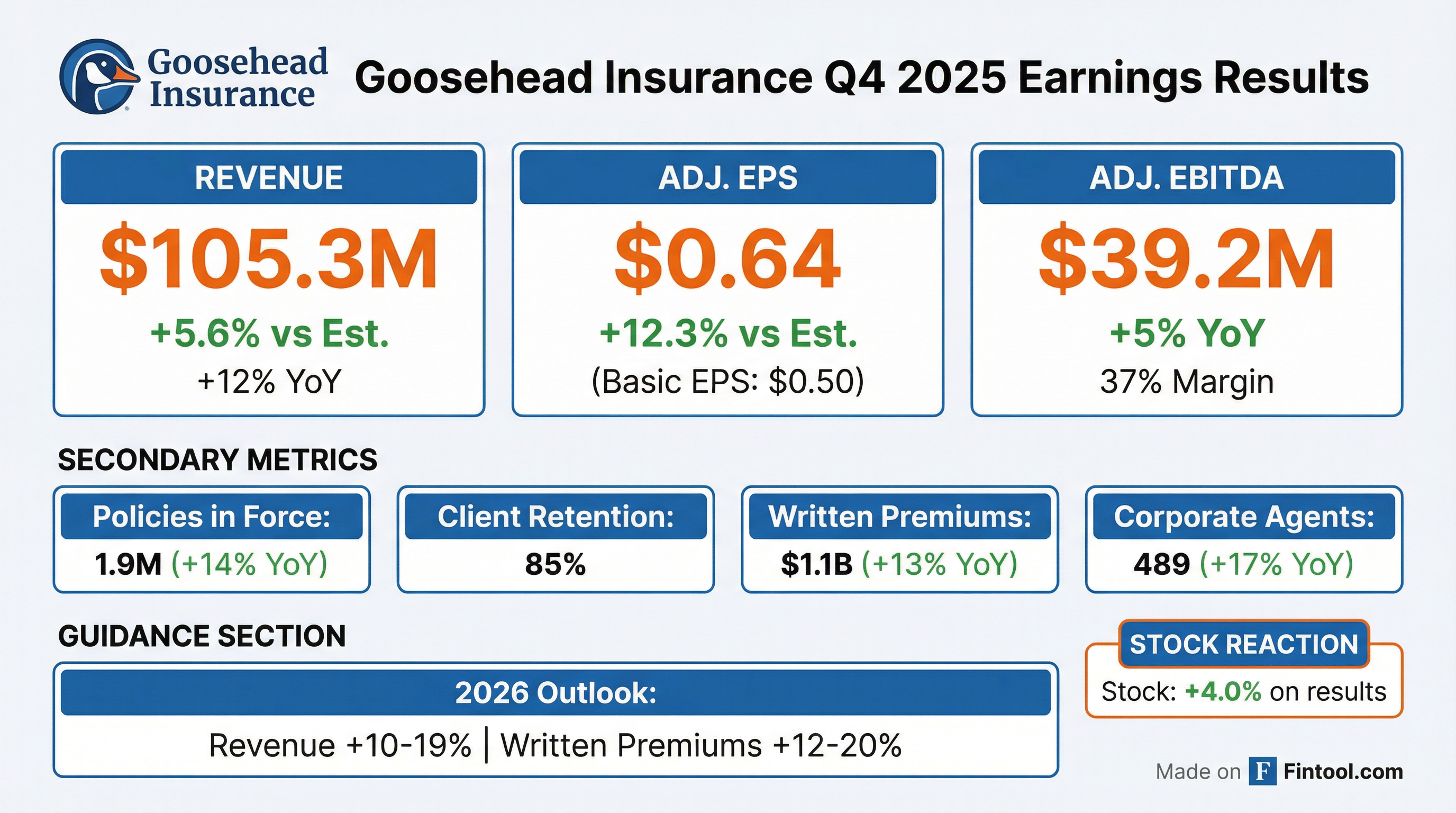

Goosehead Insurance (NASDAQ: GSHD) delivered a double beat in Q4 2025, with revenue of $105.3 million exceeding consensus by 5.6% and adjusted EPS of $0.64 topping estimates by 12.3%. The stock rose approximately 4% following the release. The quarter was highlighted by the launch of Digital Agent 2.0—what CEO Mark Miller called "the United States' first end-to-end comparative insurance digital buying experience"—and a $180 million expansion to the share repurchase program.

On the earnings call, management addressed investor concerns around AI disintermediation head-on, emphasized a "Rule of 60" long-term framework (revenue growth + EBITDA margin >60%), and revealed that 2.3 million potential clients are now in the partnership pipeline.

Did Goosehead Beat Earnings?

Yes—Goosehead beat on both revenue and EPS.

*Consensus estimates from S&P Global

Core Revenue—the company's most reliable revenue stream consisting of commissions, agency fees, and royalty fees—grew 15% YoY to $78.2 million. This outperformance was driven by:

- 85% client retention (up from 84% in Q2 2025) with continued upward momentum

- Improving product market as carriers exit the hard market and compete for growth

- Productivity gains with same-store sales up 19% and gross payments per franchise up 29% YoY

Management noted that product availability is now "pretty wide open"—auto has been fully available for some time, and home went from ~50% open toward end of 2024 to now having product available in every market.

How Did the Stock React?

Goosehead shares rose approximately 4% following the earnings release, trading at $50.63.

The stock remains well off its 52-week high of $127.99, down approximately 60% from peak levels. The Q4 beat provides some stabilization after a challenging year for the shares.

What Changed From Last Quarter?

Several key developments differentiated Q4 from prior quarters:

1. Digital Agent 2.0 Goes Live

The biggest strategic milestone was the launch of Digital Agent 2.0 in Texas with multiple auto carriers. CEO Mark Miller emphasized this represents a significant competitive moat:

"Goosehead has now delivered the United States' first end-to-end comparative insurance digital buying experience... These capabilities can only exist with deep relationships and trust with the carriers, complex integrations with underwriter backend systems, and a high-scale service organization."

On the call, CFO Jones clarified that policies have already been bound with no human involvement, and that the platform is being used by existing monoline home clients to add auto policies—actually improving retention by rounding out the account.

Home insurance carriers are in "active implementation" with multiple top carriers. The company plans a second-half 2026 Investor Day to demonstrate the frictionless shopping experience.

2. Margin Compression Despite Beat

Despite the revenue beat, profitability metrics showed pressure:

The margin compression was driven by:

- Higher interest expense: $5.7M vs $1.8M in the prior-year period

- Increased compensation: Employee costs rose to $48.9M from $45.0M

- Technology investments: G&A expenses increased to $22.1M from $17.8M

3. AI-Powered Service Improvements

Management highlighted AI initiatives that are already generating results:

- Lily — An AI-powered virtual phone assistant that has handled "hundreds of thousands of client interactions" and reduced calls requiring agent involvement

- Mobile app — Allows clients to manage policies across multiple carriers in one place

- Intelligent routing — Deployed tools to reduce complexity for service teams and create foundation for further automation

Management outlined three strategic AI focus areas: service efficiency, matching carrier risk appetite with client demand using proprietary data, and targeted marketing for retention and cross-sells.

4. Corporate Agent Expansion Accelerates

Traditional corporate sales agents grew 6% YoY to 374, while enterprise sales nearly doubled to 115 headcount. The company opened three new offices in February 2026 (Tempe, Nashville, and others) with a fourth planned for Q2.

What Did Management Guide?

2026 guidance was reaffirmed with:

Management provided additional color on the guidance range during the Q&A:

- Top end assumes continued improvements in client retention and acceleration in the second half

- Bottom end assumes pricing generally down and retention improvements stall

- Housing: No improvement assumed in guidance; would be potential upside

- First half pacing: Expect low double-digit core revenue growth as pricing headwinds and franchise consolidation weigh

- Second half acceleration: Expected as partnerships and Digital Agent 2.0 investments take hold

Strategic Investment Spending

Management outlined the investment plan driving margin compression:

CFO Mark Jones Jr. emphasized these are defined investments with expected returns, not an "infinite money pit."

Key Operating Metrics

Management addressed the NPS decline on the call, noting it's a trailing 12-month metric that still reflects early 2025 price increases. CFO Mark Jones Jr. said the company also tracks a CSAT score for individual agent interactions, which has held steady at 4.2 out of 5.

The decline in operating franchises from 1,103 to 1,009 reflects intentional franchise consolidation—stronger agencies are acquiring smaller single-producer agencies and reinvesting cashflow to add producers.

Capital Allocation

Goosehead announced an $180 million expansion to its share repurchase authorization, extending through May 1, 2027.

Management was explicit about their buyback philosophy on the call:

"Looking at the valuation of where it is today, I think it's probably safe to say we think we're undervalued, hence the repurchase authorization."

2024-2025 Buyback Activity:

- 2025: $81.7 million repurchased

- 2024-2025 combined: $145 million and ~2 million shares (~8% of Class A shares as of beginning of 2024)

- Q4 2025: 323,000 shares at $22.5 million

In 2025, the company used 80% of the full authorization, and management indicated similar aggression is likely given current valuations.

Balance Sheet Snapshot (Dec 31, 2025):

- Cash: $34.4M

- Unused Credit Facility: $75.0M (same-day liquidity)

- Term Note Payable: $298.5M

- Cash Flow from Operations (2025): $91.8M (+28% YoY)

Management noted Q1 is typically a big cash flow quarter (contingent commission bonuses get paid), providing flexibility for opportunistic buybacks.

Board Changes

Two board changes were announced effective February 18, 2026:

- Louis Goldberg joins the Board and Nominating & Governance Committee. Goldberg was a senior partner at Davis Polk for 28+ years and was recognized by Forbes as one of America's Top Lawyers in 2025.

- Thomas McConnon departs ahead of his term expiring in May 2026. McConnon served since February 2022 and is focusing on managing Whitebark Investors LP.

Q&A Highlights: AI, Disintermediation, and Long-Term Vision

Will AI Disintermediate Insurance Agents?

The most significant Q&A theme was AI disintermediation risk—a topic that's been top of mind for investors following recent industry developments. Management pushed back firmly:

"Auto generally becomes more commoditized over time... Home remains complex and often is the largest asset for our clients. I think they're going to be particular about how they buy that product."

CEO Mark Miller emphasized that Goosehead leads with the home product and cross-sells auto, making disintermediation harder. He also noted that the service function—handling complex claims and policy changes across hundreds of carriers—is a key moat:

"What makes Goosehead so unique is the size and capability of our service function compared to anybody else."

CFO Jones added that the company is the only platform that can bind policies end-to-end without human intervention: "Everybody else out there is lead aggregation."

Partnership Potential: 2.3 Million Clients

Management revealed that partners on the platform now represent 2.3 million potential clients across mortgage origination, servicing, and other financial services—with the majority still in implementation phase and not yet generating lead flow.

"The majority of that partnership base is still in the implementation phase, meaning the benefits from those arrangements are not yet felt in our financial results... Ultimately, we expect the partnership business, in tandem with the digital agent platform, have the potential to be the single largest growth driver in our company's history."

Rule of 60 Aspiration

President Mark Miller articulated the long-term financial framework:

"We believe Goosehead has the ability to operate at a rule of 60 model over time, with a combination of revenue growth and EBITDA margin exceeding 60% on a sustained basis."

Franchise Consolidation Timeline

When asked how long franchise consolidation would continue, management indicated 12-18 months from the Q3 2025 call, meaning it may extend into early 2027. However, they view this as value-creating—acquiring agencies are in the top 5% of production and the system is getting stronger overall.

Geographic Diversification

Texas concentration declined from 40% of full-year premiums to 38% for Q4, reflecting a deliberate effort to diversify geographically. The company expects this trend to continue.

Full Year 2025 Results

What to Watch Going Forward

-

Digital Agent 2.0 expansion — Management plans to expand product and market coverage rapidly after the Texas pilot. Home carriers are in active implementation. An Investor Day webcast is planned for the second half of 2026 to demonstrate the platform.

-

Partnership activation — With 2.3 million potential clients in the partnership pipeline, execution on implementation will be a key value driver. Only a "pretty small percentage" is live today.

-

Retention trajectory — Management looks at retention "down to two decimal points" daily and expects it to continue improving as pricing stabilizes.

-

Franchise consolidation completion — Expected to extend into early 2027. Will result in fewer operating agencies but higher productivity per franchise.

-

Commission rate recovery — Franchise commission rates have declined over a point since 2023. Management called this "a big area of focus" as carrier profitability has improved.

-

Corporate sales expansion — Three new offices launched in February 2026, with a fourth planned for Q2. Management expects headcount to grow (though not double) in 2026.

Related Links: